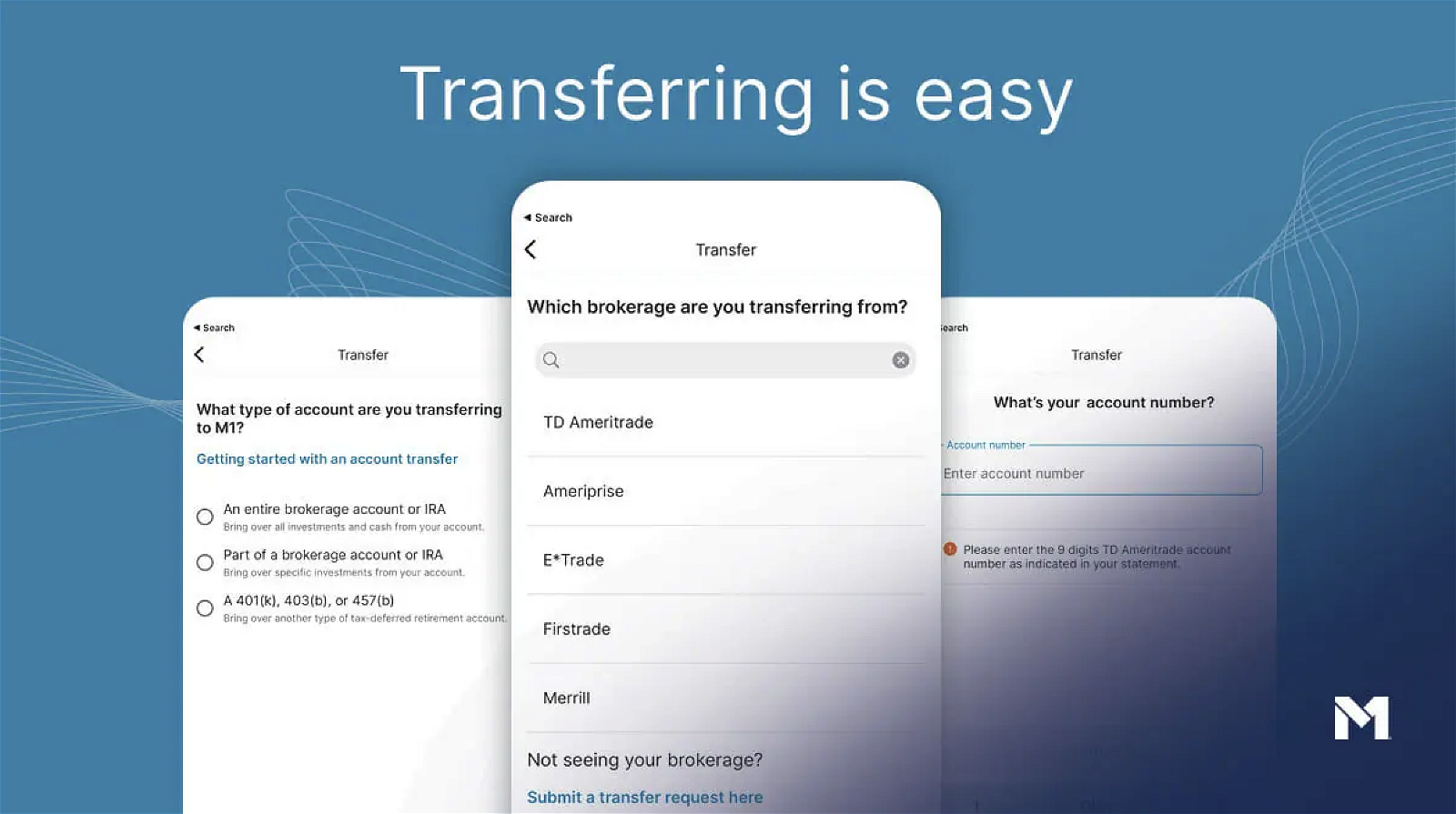

|

Insights: How you can build a portfolio for yourself, and meet your financial goals — from an M1 employee who did it himself

I gave myself two extreme goals in my early twenties. I wanted to pay off my \\$80,000 in student loans, as well as build a six-figure investment portfolio before I turned 30. I set these goals intentionally to clear away this massive pile of debt so I could move on to other ventures like buying a home, as well as give me the flexibility to potentially retire with a large nest egg.

If you have lofty financial goals, it may take some creative ideas and persistence. But with the right plan, you give yourself a great chance of reaching those milestones. Here’s how I was able to hit my goals:

I took on side hustles like freelance writing and grocery delivery to pay down the student loans even quicker. Some months I made a few hundred dollars, while others, I made several thousands. All of this money went towards my student loans. I alsorefinanced my student loans multiple timesto cut down the interest rate I paid on them. This easily saved me thousands of dollars in interest by simply shopping around my interest rate on a regular basis. However, this may not be the right plan for everyone.

I cut back on my expenses significantly by living with roommates and even went without a car for several stints.

And lastly, I job-hopped regularly to jump my income. Since the beginning of my career, I have been able to almost quadruple my full-time income by regularly searching for higher paying work to hit my financial goals. This strategy was non-conventional, but it worked for me. However, job hopping can be stressful and may not be for everyone.

When I started investing, I was investing in my Roth IRA, employer-sponsored 401(k), health savings account (HSA), and a taxable brokerage account. I focused on the first three accounts as they each offer their own level of tax incentives. The HSA has a triple-tax advantage, giving investors the opportunity to invest funds tax-free, allow them to grow tax-free, and potentially withdraw them tax-free.The Roth IRAallows your post-tax funds to grow tax-free for retirement, and your 401(k) allows you to defer your tax liability until you hit retirement.

Pro tip: Check out the difference between an IRA and taxable brokerage accounthere.

Once I hit my contribution limit for these accounts, I moved onto my taxable brokerage account. It’s not the fanciest strategy, but every time I had a few hundred dollars extra, I threw it towards the bucket I needed to fill based on the tax benefit.

Despite the pandemic and several personal life events, I paid off my student loans inOctober 2022. It was like a monkey had fallen off my back. And once I paid them off, I was able to redirect those student loan payments into my stock portfolio. Six months later, I hit the glorioussix-figure club— seven months before my 30th birthday. |

Here are the takeaways I’ve learned of building a six-figure portfolio before 30 years old- Financial goals are imperative.The strategy I used is to set a realistic goal that I confidently believe I could reach and take it one step further. You’ll be amazed at what you can accomplish when you push yourself.

- Consistently buying despite your emotions.It can be easy to neglect investing and put it off until tomorrow. I’ve foundautomated investing, as well as consistently throwing money into my investments has been the best strategy for my goals, regardless of the current market circumstances.

- Sacrificing for a better tomorrow.Investing for me has always been about sacrificing my wants today for a better tomorrow. So while I’m tempted to splurge at times, staying consistent on my investing journey will provide me financial flexibility later on in life. For example, I was recently searching for a car and was extremely tempted to get aTesla Model 3.However, because of the cost, I decided to get a simple Honda instead, and invested the difference between the two cars.

|

When I first startedhammering away at my goalsin 2017, I felt like I would never reach the mountain top. The 2018 stock market correction followed by the 2020 pandemic recession made it feel nearly impossible. In fact, there’s a Charlie Munger quote (I’m paraphrasing) stating that the first \\$100,000 of investing is always the hardest. And this couldn’t be more true.

While this strategy has worked for me, it’s not the right strategy for everyone.

-Brett Holzhauer, Content Marketing Manager at M1 |

| Q&A: What are the benefits of self-clearing? And when will it be rolled out to more users?

A:Self-clearing gives us more control and allows for faster updates and improvements to the M1 platform in the future. It also brings platform connections between M1 products.

We recently completed our second wave of current users accounts. We will complete one more wave in the next few weeks, and then all individual taxable accounts will be on our self-clearing platform. |

|

|

|

| Wake us up when September ends

The turn of the calendar into September is exciting. Football is back. The weather may start cooling down by a few degrees. The leaves in your yard may start turning shades of red.

But that red in your trees unfortunately could be a sign of your portfolio over the next few weeks. Historically (but not always), September is the worst month for the S&P 500, a phenomenon known as the “September Effect.” |

|

|

|

Thanks for choosing M1,

The M1 Team |

|

| \t \t\t\t\t\t| \t\t\t\tDownload the M1 app | \t \t\t\t\t\t\t\t\t\t | \t\t\t\t | |

\t This is an automated message, and we will not receive your response if you reply. M1 is a technology company offering a range of financial products and services. “M1” refers to M1 Holdings Inc., and its wholly-owned, separate affiliates M1 Finance LLC, M1 Spend LLC, and M1 Digital LLC.

\t

\tM1 newsletters reflect the opinions of only the authors who are associated persons of M1 and do not reflect the views of M1. They are for informational purposes only and are not a recommendation of an investment strategy or to buy or sell any security in any account. They are also not research reports and are not intended to serve as the basis for any investment decision. Prior to making any investment decision, you are encouraged to consult your personal investment, legal, and tax advisors. Any third-party information provided therein does not reflect the views of M1.

\t

\tAll investments involve risk including the loss of principal and past performance does not guarantee future results. Brokerage products and services offered by M1 Finance LLC, MemberFINRA/SIPC.

\t

\t© Copyright 2023 M1 Holdings Inc. |

|

|

|

|

|

|